R1 Expressway refinancing, Slovakia

On 29 November 2013 the Granvia Consortium, project sponsor of the R1 Expressway in Slovakia, reached financial close on a €1.24 billion (US$1.7bn) bond issue to refinance outstanding debt on the PPP project. The R1’s bond refinancing was over-subscribed, with half the bonds placed to European institutional investors. It is the largest unwrapped, non credit-enhanced issue for a PPP in Europe.

The project

The R1 Expressway was the first PPP in Slovakia when it reached financial close in August 2009. The 51.6km dual-lane road links Slovakia’s two largest cities – Bratislava in the west and Kosice in the east – and provides vital access to the country’s borders.

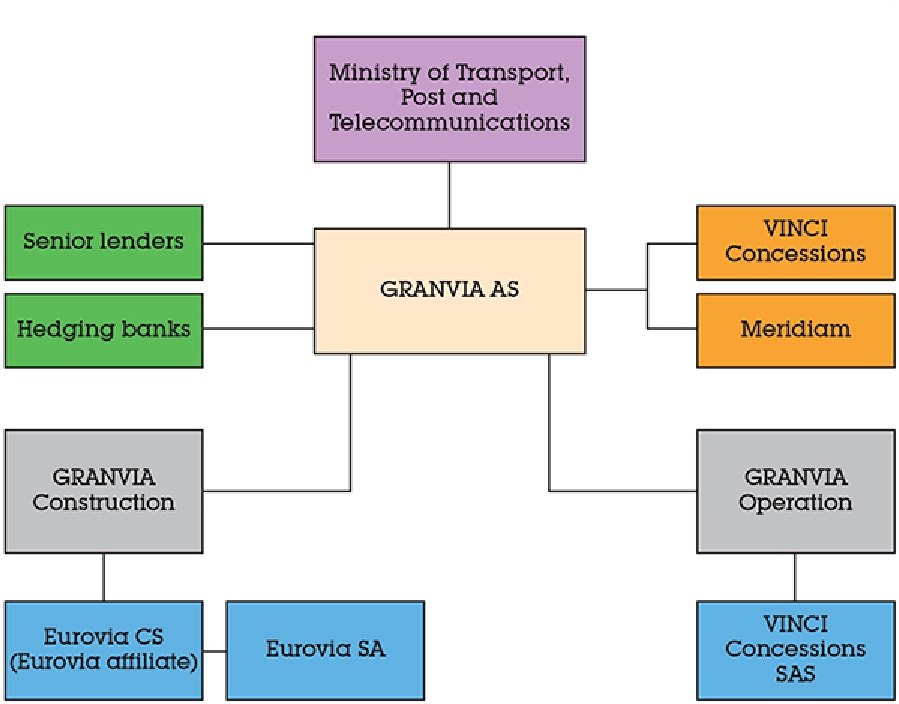

The Granvia Consortium, made up of Meridiam Infrastructure (50 per cent) and Vinci Concessions (50 per cent), was named preffered bidder on the project in December 2008. The 30-year post-construction design, build, finance, operate and maintain concession was awarded by the Slovak Ministry of Transports, Posts and Telecommunications (MTPT).

The project is divided into four sections: three form a 45.9km continuous road from Nitra to Tekovske Nemce, while the fourth is a 5.7km bypass around Banka Bystrica.

The project sponsors and MTPT had been disputing the project’s penalty regime for availability payments since the first section of the road was completed in 2011. The ministry imposed penalty deductions above the concession’s termination thresholds, and disagreements covered oil separators, de-icing materials and the submission of an annual maintenance plan.

The construction contractors were obliged to pay liquidated damages, but the project continued to meet debt service and the disputes did not escalate into litigation. The road became fully operational in September 2012 and following a memorandum of understanding between sponsor and authority, the government started making availability payments on 1 November 2013.

The memorandum confirms a base availability payment of €125.4 million per year from the grantor, 10 per cent of which is indexed. The maximum penalty or bonus in any year is €2 million for safety-related issues, and deductions up to €5,000 per month for each penalty point. The road must meet minimum availability of 80 per cent to avoid termination and the concessionaire has a maximum of 300 penalty points per year. But the concessionaire can terminate its operations and maintenance contract at 225 penalty points per year and a minimum of 89 per cent availability. Vinci Concessions is the O&M contractor.

The financing

On 22 November 2013 Granvia priced €1.24 billion of bonds, which listed on the Luxembourg Euro MTF market. They priced at 235bp over mid-swaps for a 4.781 per cent coupon that is paid semi-annually. The bonds mature in 25 years and eight months, and fully amortise two years before the concession ends. The bonds benefit from a six-month debt service reserve account. Standard & Poor’s rated the bonds BBB+. Deutsche underwrote €900 million of the bonds, while Natixis was also a bookrunner. The bonds priced at the bottom end of the leads’ range and attracted €1.4 billion of orders.

The November bond issuance refinances the €984 million in 2009 bank debt, which featured the EBRD and a large commercial bank club. The bond issuance will refinance €973.1 million outstanding on that debt and pay interest rate swap breakage costs of €210.5 million. Deutsche provided a hedge from when the bond priced on 22 November up to the close of documentation, funding and offsetting on the swap, which took place a week later. An existing subordinated sponsor loan of €146.8 million and pure sponsor equity of €2.3 million remain in place. The leverage on the new package is 89 per cent.

Below is the contractual structure for the R1 PPP:

Investor breakdown

About 30 accounts participated in the bond issue, broken down as follows:

Investor type:

- Institutional investors - 51 per cent

- Banks - 24 per cent

- Multilaterals - 16 per cent

- Asset managers - nine per cent

Investor location:

- Germany - 34 per cent

- UK - 24 per cent

- Slovakia - 11 per cent

- France - nine per cent

- Switzerland - seven per cent

Of these investors KfW and EBRD, who were both orginial lenders on the 2009 financing, invested in the bond. KfW took a €150 million ticket. EBRD took a roughly €200 million ticket. Erste Bank, another lender on the original financing also invested in the bond issue.

Investor appetite

Deutsche held road shows in London, Paris and Zurich, along with MTPT officials, which reassured potential investors about an imminent resolution to the disputes about the projects penalty regime for availiability payments. At the time, problems with the Castor underground gas storage project were casting a shadow. Castor had priced its €1.4 billion in bonds at 100bp over its government benchmark on 25 July, but after seismic tremors delayed acceptance on the facility its bonds were trading at closer to 250bp.

The MTPT had set a minimum debt service saving requirement for the bond issuance to go ahead, and the sponsors retained the option of closing a short-term bank financing or maintaining the original debt. The average debt service coverage ratio was 1.35x under the original debt package, with S&P assessing it at a base case 1.27x after the refinancing.

The asset has few comparables and interest and pricing expectations varied hugely. More marginal and local investors were prepared to go close to the sovereign, but many European investors with a strong understanding of PPP were hoping for wider pricing.

The sponsors’ track record helped attract commitments. Both are serious PPP players and Meridiam was a sponsor of the L2 Marseille PPP, which issued €164.5 million of bonds in October 2013. The L2 bonds were also unwrapped, although in that case they financed a greenfield project and were placed to a single buyer – Allianz.

Investor appetite for long term PPP debt exposure has been strong this year, with pension funds and insurance companies accounting for much of the demand. Slovakia’s experience in resolving issues between concessionaire and government will help it procure other strategic road projects in early development.

Advisers

Deutsche Bank was financial adviser to the issuer. HSBC was financial adviser to the grantor. Linklaters was legal adviser to the sponsor. Allen & Overy was bookrunner's legal adviser. Ashurst was legal adviser to the grantor. Atkins was technical adviser.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.