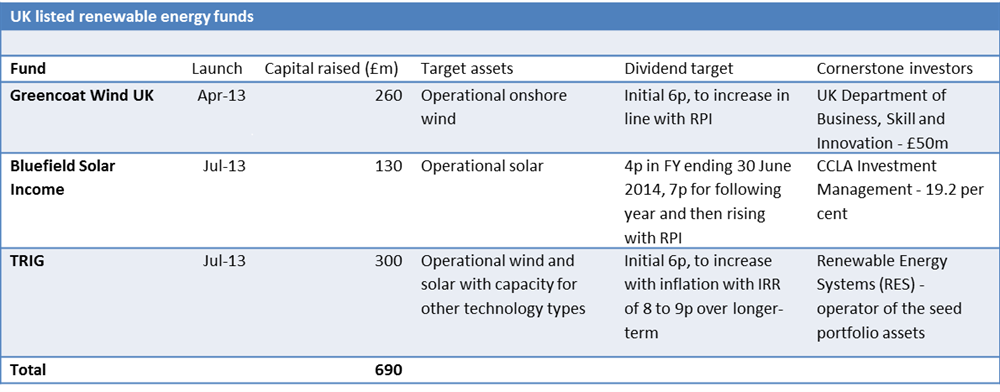

News+: UK listed renewable funds

There’s no doubt that listed infrastructure funds have always played second fiddle to their unlisted counterparts, which evolved out of the private equity model, both in terms of size and market share.

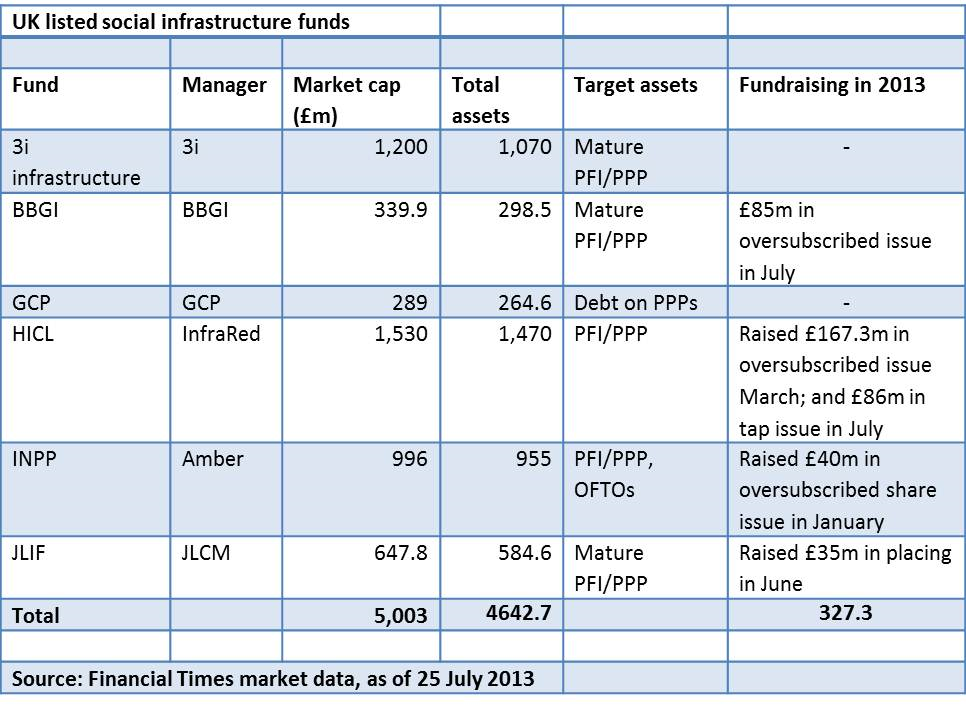

The six social infrastructure funds traded on the London Stock Exchange have a combined market capitalisation of £5.03 billion (US$7.72bn) – a tiny fraction of the US$231 billion raised in the last decade by closed-end, private funds, nearly half of which was secured by 10 GPs, according to data from Preqin.

But the listed market is showing signs it can be a suitable home for the generation of operational renewable energy generation assets that is coming up for sale in the UK. Amid a run of successful equity issuances by the existing listed funds, this year has witnessed the debut of a handful of renewable managers on the LSE main board.

In April came the flotation of what was said to be the first fund dedicated to renewables, Greencoat Wind UK, which after more than a year in gestation pocketed an impressive £260 million in an oversubscribed share sale.

It was followed this month by Bluefield Solar Income, which far surpassed its minimum initial public offering (IPO) target by raising £130 million.

And just this week, InfraRed, the manager of well-established listed social infrastructure fund HICL, raised £300 million from the capital markets for its mixed renewables fund TRIG – again, beating expectations of investor interest.

In each instance bookbuilding was given a helping hand by cornerstone investors making substantial orders of shares.

Part of the allure is yield. With government bonds still yielding historically low and equities volatile, many investors are seeking an alternative form of income, says Charles Cade of Numis, which acted as broker for the Bluefield launch.

“The attraction of wind and solar is where you have government-backed revenue in the form of feed-in tariffs (FITs) with an inflation linkage,” he told IJ News.

In contrast to the typical unlisted infrastructure fund, most of whose LPs are pension funds and insurance companies, a large proportion of the investor base of the listed renewable funds is multi-asset managers and wealth managers.

“They need a daily valuation of their portfolios and certain liquid criteria which is possible in the listed market,” Cade added.

Private funds have for several years invested in renewable energy – Zouk, Glennmont (spun out from BNP Paribas earlier this year) and Impax are the most notable – but some analysts say that operating assets are better suited for the listed market, which cannot tolerate the yield lag associated with greenfield developments. Fees also tend to be lower than in a private equity-style structure.

By virtue of enjoying a government-backed revenue stream, a key selling point for all three renewable listed funds is the similarity their underlying assets share with social infrastructure projects, such as hospitals developed through the private finance initiative (PFI) – though predicated on a slightly higher risk and return. Not only do FITs rise in line with the Retail Price Index (RPI), but the subsidy means that renewable power generators will not be fully exposed to the fluctuations of the wholesale electricity market.

Greencoat for example derives half of its revenues from similar “green benefits” in the form of index-linked Renewable Obligations Certificates (ROCs), which it says provides sufficient dividend cover. The company adds that exposure to wholesale prices is actually an upside should prices increase above expectations.

TRIG, which will buy assets across northern Europe, similarly intends to limit its exposure to merchant power prices through a combination of FITs, long-term power purchase agreements and green certificates.

Unlike its two peers, Greencoat will only buy unlevered assets, meaning no financial risk at the asset level with only some electricity price risk. This is particularly important given the variability of wind speed. If there is a repeat of the low levels felt in 2010, a drop in generation by an asset can lead to ‘lock-up’, in the event that borrower covenants are broken. In effect the equity is punished as dividends cannot be withdrawn for up to two years.

Many energy utilities are financially distressed and therefore unwilling to put the liability of a fixed price, long-term power purchase agreement (PPA) on their balance sheets. The absence of these could thwart the typical private equity model of buying an asset and leveraging it up with cheap debt to maximise equity returns in the first place, as few banks are willing to lend in the volume and price risk scenario.

On the asset supply side, many utilities are looking to divest their operating wind assets and recycle the capital back into new projects to meet the government’s target of 15 per cent renewable by 2020. In solar, developers tend to be smaller but many are too looking to exit.

A pre-arranged agreement with SSE and RWE saw Greencoat fully invest its capital within five hours of listing and the managers’ prior experience in the asset class bodes well for future dealflow.

The majority of TRIG’s asset pipeline comes from its operational manager Renewable Energy Systems (RES), with the balance made up from other InfraRed funds, although this does leave questions of conflict of interest.

Bluefield on the other hand will have to battle it out with the raft of general infrastructure funds with dry power and institutionals going direct, which presents a risk over getting the best value for money while cash sits in a box.

It appears that these first three funds have, to an extent, cornered the market – both in terms of securing cornerstone investors and hunting assets while competition remains relatively low. Greencoat’s team have involvement in the financing of many renewables deals, putting them in a strong position for sourcing assets in a market they estimate will be worth £40 billion three years’ time. While political risk in the form of adverse regulatory reform can never be discounted, UK renewables appears an area ripe for more secondary investors.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.