University of Hertfordshire, UK

Student accommodation is one asset class that has caught the attention of a variety of investors in the UK over the last two years.

Most of the deals that reached financial close in the sector last year were largely financed with long-term debt from investors like Aviva. The University of Hertfordshire student accommodation project, however is unique in the way it has been financed. Most notably, it is the first deal in Europe to be financed using a bond solution right from the construction phase. It sets a good blue print for rest of the projects in the sector and signals growing interest from institutional investors in the asset class.

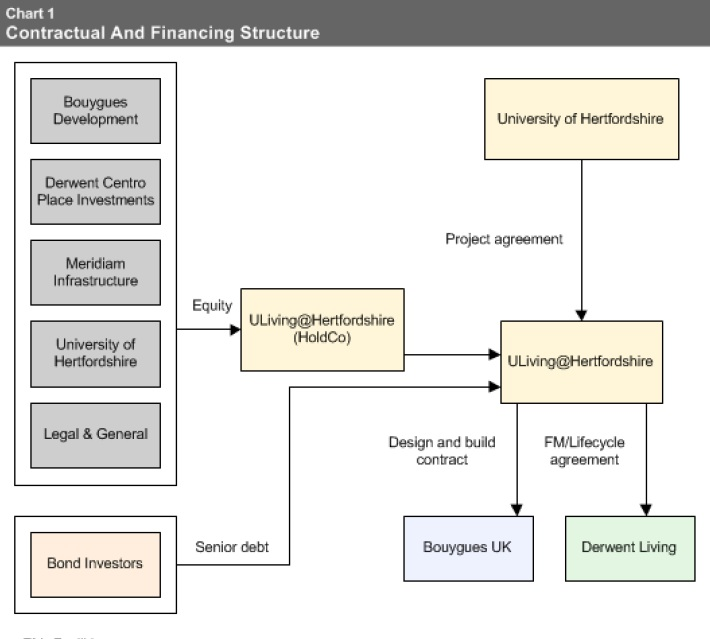

The University of Hertfordshire and the ULiving Consortium, comprising Bouygues Development and Derwent Living, reached financial close on the £190 million (US$296m) student accommodation project in May this year using a bond solution to finance the project. Further, the funding has been arranged through an index-linked unwrapped private bond placement.

Renewed interest in bond financing also reflects the growing influence of shadow banking in the infrastructure sector generally. It is also telling of the fact that institutional investors may not be that wary of construction risk after all as the project received an investment grade rating pre-completion.

Project Scope & Financing

University of Hertfordshire tendered the student homes project in 2011 and chose the ULiving Consortium, comprising Bouygues Development and Derwent Living, as preferred bidder a year later in July 2012. The project reached financial close in May 2013.

Located at the College Lane campus in Hatfield, the project is part of the University’s vision to enhance students’ lives by creating a fully inclusive living and learning campus environment. Under the scheme, Uliving will be responsible for the design, build, finance and operation of new student accommodation totalling over 3,000 bedrooms, and the associated social spaces and infrastructure works.

Bouygues Development will manage the development and construction management of the project. Derwent Living, again as part of the Uliving consortium, will be responsible for the operation and facilities management elements of the contract for a total period of 50 years. The operation and facility management tasks will begin immediately to cover the existing student accommodation.

Construction, which involves the development of over 2,500 new bedrooms before September 2016, will be undertaken by Bouygues UK under a contract worth ca. £117 million. Derwent Living’s provision of asset management and facilities management services for the new and existing units will be worth more than £200 million over the lifetime of the contract.

Derwent Living will also refurbish the existing 500 bedrooms over the next three years. The scheme will be delivered in three phases with the first phase due to commence immediately and is scheduled to be completed in September 2014 in readiness for the start of the new 2014/2015 academic year.

Each subsequent phase will be completed in time for the start of the following academic year with the entire scheme being completed in September 2016. Construction works will run alongside the existing accommodation units, which will be transferred to Uliving immediately and be in full operation throughout.

In addition to the main construction and refurbishment works, the scheme includes new sports pitches, a campus gym, informal learning and social spaces and a new dedicated bus route.

The project has been funded via an index-linked unwrapped private bond placement. ULiving will issue £143.5 million of senior unsecured bonds, due to mature on 31 July 2054. The bonds are being placed by RBC and UK insurance company Legal & General will buy all of the bonds issued. The senior secured bonds have been assigned a preliminary 'A-' rating by Standard & Poor's with a 'stable' outlook.

As mentioned earlier, a major highlight of the financing is that it is the first deal in Europe to be financed with a bond solution right from the construction phase reflecting the fact that institutional investors are not shying away from construction risk, if of course the asset is worthwhile.

"We like student accommodation as an asset class, it has intrinsic stability," says Georg Grodzki, head of credit research at Legal & General Investment Management. He added that they are pleased to have done the deal and that they remain committed to the sector.

Grodzki agrees that construction risk is a manageable risk for investors like them. "It is a myth in the market that only banks take construction risk." He says that not every type of construction risk is acceptable for investment grade investors but in this instance the risk was well mitigated.

He also said a decision in favour of a bond solution was made at an early stage in the process and that the main motivation was to have maximum flexibility with respect to the placement of the transaction.

Another investor in the project told IJ that the attractiveness of the bond issue was driven by the merits of the project. "The university itself is a well-established one, it is oriented towards engineering and has good prospects for students who choose to study there," the investor said.The project has the following equity partners:

- Meridiam Infrastructure Finance II (55 per cent)

- Bouygues Development (13.3 per cent)

- Centro Place Investments, a subsidiary of Derwent Living, (13.3 per cent)

- University of Hertfordshire (13.3 per cent)

- Legal and General Assurance Society (five per cent)

In almost all student accommodation projects, the main risk from an equity investor’s point of view is occupancy risk i.e. level of occupancy and room rent. Equity investors in this deal are understood to have been conservative on both accounts. They took into account the lower ‘summer time’ occupancy compared to other times of the year when sessions start and occupancy is denser when pricing the project.

In its ratings report, prior to financial close, Standard & Poor's said that they see strong long-term demand for on-campus student accommodation at UoH, low construction risk, and a more robust financial profile than other similar projects in the sector. "The stable outlook reflects our view that construction work will be completed to specification, on time, and within budget, and that demand for the project's accommodation and the creditworthiness of the key counterparties will remain stable," the report said.

Unwrapped issue

The rating agency is of the view that the demand risk with the UoH is positive in terms of student demand. The overall demand for student accommodation is also very strong, the agency said. The fact that the bond was unwrapped (i.e. there is no monoline insurer guarantee) also displays the trend that the market is looking to move forward without monolines.

The A- rated bond issue is also supported by the fact that, "The transaction's more conservative structure than typical private finance initiative (PFI) projects, with leverage of 76 per cent, compared with 80-90 per cent for comparable PFI projects at the same rating level. The minimum and average DSCRs--excluding interest income as per our criteria, and reflecting our base-case occupancy and rent projections--are strong at 1.59x and 1.75x, respectively," Standard & Poor's stated in its post sale report.

"We also forecast that the coverage ratios will increase gradually over time, which should provide a cushion for revenues and operating uncertainty in the long run," Standard & Poor's added.

UoH is also an equity holder in the project and that is a positive since the university will then have an interest in keeping occupancy high. The building contract also benefits from a parental guarantee and a 12.5 per cent on-demand, unconditional, and irrevocable performance bond from Societe Generale.

Largely, the deal makes a good case for financing future student accommodation projects in the UK, although it is worthwhile to note that not all deals share the same risks and future prospects. While investors are getting comfortable with construction risks and familiarising themselves with the asset class, not all projects will be like the University of Hertfordshire, so investment will still be on a case-by-case basis.

Advisory roles

For the authority, DWPF provided financial advice and Jones Lang LaSalle gave property advice.

For the sponsors, technical advice was provided by Davis Langdon, RBC gave financial advice while legal advice was given by Trowers & Hamlins. Lenders were given legal advice by Simmons & Simmons.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.