It’s not “going to be fine” – you fool

When the bell sounds, you better know for sure whether you’re inside the ring or outside of it for the fight of the century – a grudge match of monumental proportions that will first be staged in the UK.

If you’re inside the ring, it’s time to dust off your finest Whistle & Flute and dry clean the tie you bought in 2019 – get ready for your day in court.

If you’re ringside, wear something that wipes clean because blood will fly and there’s a good chance we’ll witness another disaster of Carillion proportions.

As one infra fund manager with a hearty (not healthy) exposure to UK PPP assets puts it: “This is a 2008 moment for PFI.”

Another estimates the risk to PPP-focused infra funds at a cool £5-10 billion as the government limbers up for a cash-grab that could bring the whole stack of cards tumbling down.

Let’s take this down the data line – coz you’re all suckers for a bit of data.

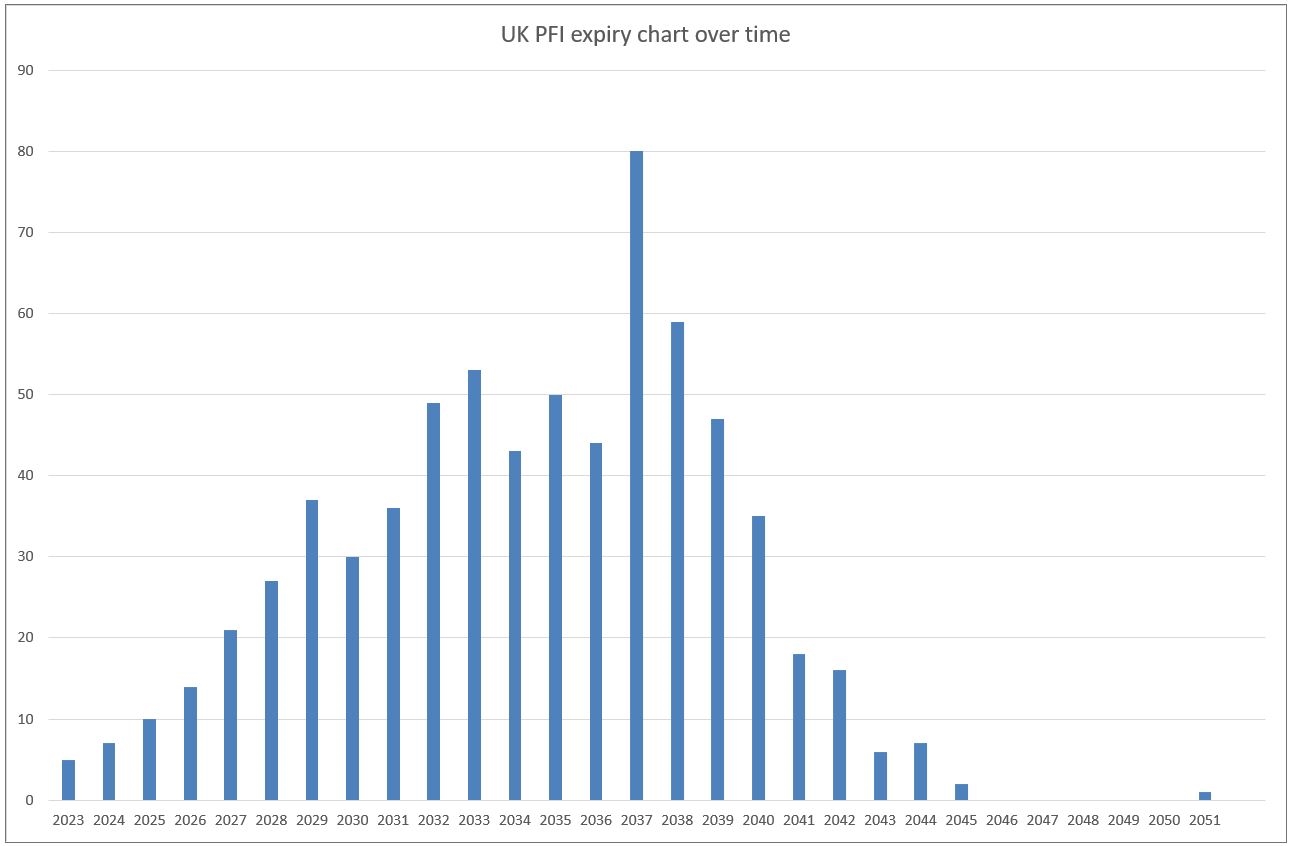

This chart (pictured right) comes to you direct from the UK Government. For of those of you watching in black in white – this HM Treasury chart shows that for 2023 alone 5 PPP projects in the UK will reach the end of their concessions. In 2024, that maturity rate rises to 7 projects; growing to 10 in 2025; 14 in 2026… you get the picture.

It rises steadily – with a couple of dips due to deal cycle – to a high of 80 PPP deals being handed back to the public sector in 2037, dropping to 59 the next year; 47 in 2039; 35 in 2040; tailing off from there to 2 in 2045 with 1 outlier in 2051.

For those wondering which PFI deal runs to mid-century, that’s the hospital procured by Oxleas NHS Foundation Trust (London) that reached financial close at the end of 1998 with a staggeringly-long concession of 50 years.

Relying on government data – not what we like to do, but a lot of the early data pre-dates the IJGlobal database – the UK has 717 closed PPP transactions (I thought there were more) and in the next 5 years (2023-28 inclusive) that amounts to 84 transactions to be handed back.

Vickerstaff’s Vanguard

OK – so there’s been a bunch of wibbling by the infra press about handback (intoned à la Lady Bracknell)… but this one doesn’t wail about the challenges of digitising video cassette recordings and bemoan dust allergies from retrieving tattered documents from rat-infested cellars.

This is a focus on the impact of debt tails, the risk to infra funds (many of them funded by our pensions) and the SPVs that run them.

In the early days of PFI in the UK, it was common practice to have a decent tail on the debt which, at the turn of the century weighted in at 3 years (sensible lending). As the market matured and competition ramped up, this scaled back to 2 years (still adequate).

However – as the sector matured and people started to do increasingly foolish things – this was slashed back to 6 months… and, while not everyone agrees, I’m sure I remember some at just 3 months.

Now here’s the rub… it’s during the tail – when you are not paying off the debt – that the investor gets much of its return.

Crocodile tears tumble as tabloid-reading morons rub hands with glee in anticipation of “fat cat” infra funds being pillaged by government. Couldn’t happen to nicer people and all that guff. The realisation that their pension fund is heftily invested comes later.

Pause now and ponder why HM Treasury’s Infrastructure and Projects Authority (IPA) – Vickerstaff’s Vanguard – has been staffing up so vigorously in recent time. And continues to staff up. You can’t go on LinkedIn without seeing an IPA job being advertised.

From Nick Smallwood who started as chief executive in July 2019 through to SocGen veteran Matthew Vickerstaff who has been in place since 2016, that’s your top brass. It keeps on going… Jon Loveday joined as director of infrastructure, enterprise and growth in July 2020 (most relevant recent experience at Thames Water where he was a transformational director); Helen Campbell joined in May 2021 as the director of strategy, performance and assurance seeking to improve “project delivery capability” (ex National Grid director of strategy and performance); Jo Jolly who came on board last October as head of project futures, and is a bit of a data guru.

Those are just the ones we reported on (slow news days).

You can add to that list the likes of the ever-charming Jay Doshi of Amey fame (don’t mention Birmingham); the impeccable Nick Iliff who has been at more law firm than I care to mention; Jo Fox and Shona Henderson, both of whom bear the scars of the Big 4; Ian Gardner who cut his teeth at the MoD PFI unit (probably mates with Nick Prior); and Rachel Nodder who was at RBS until 2007 (just before boxes and potted plants) and has been at Whitehall ever since.

And there’s more… serried ranks of them. Feel free to spend the rest of the afternoon trawling through LinkedIn and stare in wonder at the number of technical advisers, lawyers and accountants.

And the team keeps building. So what’s the plan?

Well, it’s obvious – if the asset owners have cash at risk… government has the potential to gain.

And our charming government (which relied on the private sector to take the nation’s infrastructure from Victorian hell holes to modern facilities) has caught the scent of a few bucks to be made.

Bayonetting the wounded

This sub header is prompted by a WhatsApp response from an old chum on hearing the thesis for today’s editorial: handback gathering pace, debt tails proving troublesome, government going all-out to claw back every penny it can, impact on infra funds and operators.

The response was immediate that the IPA is “bayonetting the wounded in the battlefield” and, not satisfied with that level of imagery, rounded off with “heroic stuff”.

Essentially, the public sector is up-skilling (plastic sheeting laid out for future blood-letting) while the private sector de-skills at the most crucial point for the UK PPP industry which has the best part of 28 years yet to play out.

First, the debt. The beauty of a long tail (just ask a macaque) is that in the final months there is no debt to service and the returns go direct to equity… while continuing to operate the facility (obvs). The requirement not to pay down loans frees up cash to return the facility to its original state and – let’s be honest – provides a return for the investor who shouldered all the risk throughout construction and operation. This is when the true equity return kicks in.

The motivation for lenders to be out of the deal before the dying days of the concession is obvious, and their goal is not to be in the room when the surveys are carried out towards the end of the concession period and deductions are negotiated prior to handback.

This is when the now seasoned veterans of the infra lending community (probably wet-behind-the-ears juniors at financial close) take to the dock in a dusted-off suit and starchy necktie to field the all-important question: “Can you please explain why – in this lengthy contract – there is only one paragraph pertaining to the handback of this asset?”

From what we hear, early PPP contracts boast a single paragraph on handback stating something along the lines of: “The asset will be handed back in accordance with Condition XYZ.”

It’s a crying shame that more thought was not given in those contracts to the handback phase and the reasons why this did not happen are so human that they’re LOL-worthy.

Bottom line, most folk who worked on them thought they’d be dead by the time any questions were asked. If not dead, at least long retired (possibly thinking of a non-extradition country right now).

That’s a bit flippant. Perhaps it’s better to bring it back home. When you take out a mortgage you don’t think ahead to when you clear it. It’s so far down the line that it just never occurs to you to plan that far ahead.

This lack of clarity has given the government justifiable reason to ask questions… and set up a body – Vickerstaff’s Vanguard – to ensure that it’s getting a good/fair deal (good and fair being subjective relative to which seat you occupy). And to achieve that goal, the IPA has created the Centre of Best Practice readying itself for the flood of handbacks.

One of the key changes the IPA has made is to bring forward asset surveys from 2 years prior to contract expiry to… 7 years before termination. You better believe that caught the lenders’ attention and had investors sitting up straighter.

The motivation for Vickerstaff’s Vanguard – government really – is quite right and as a taxpayer in this country, you have to support it. The goal is to ensure such emotive assets as schools and hospitals are returned in tip-top condition and the government is seen to have done everything in its power to achieve its goals.

Just as the hangman’s noose focuses the mind, the approaching termination of PPP contracts is starting to be viewed by investors in a very different light as it reassesses unrealistic expectations for returns.

As one source says: “Investors need to wake up to the reality that the valuations that PFI assets are currently at… well they aren’t going to deliver.”

Another says: “This phase at the backend of handback has a lot of people worried. We reckon that 60% of our assets – as a baseline – is at risk. Our investors aren’t thinking like that, other investors aren’t thinking like that, and valuers aren’t thinking about that either. But suddenly people are going to start twigging it and suddenly investments will have to be written down.”

A shiver runs down your spine. Lawyers step out of darkened doorways. VCR players are acquired from charity shops. Juniors take time off work from dust inhalation. Investors straighten their ties. And schools keep churning out workplace cannon fodder and hospitals keep on doing what they do. The world continues to turn.

But even given all the above, if you have a portfolio of UK-based PPP assets and you took it to market right now… they’d be tripping over their feet to buy it.

Go figure.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.