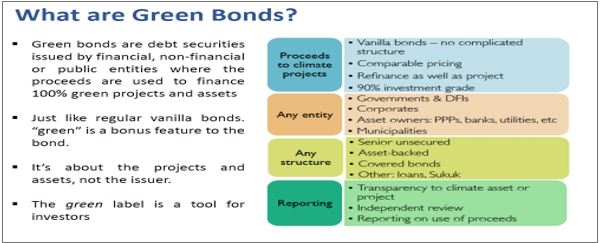

Green bonds – bridging the infra funding gap

Guest writer: Paul D Clifford, Adjunct Professor, Columbia University, New York

Debt capital markets and project bonds represent one of the keys to unlocking the flow of long-term yield chasing western institutional capital needed to address this infrastructure gap. One of the most exciting developments in this space in recent years has been the growth in green project bonds targeted at climate impact reduction infrastructure investments.

Source: Climate Bond Initiative (CBI)

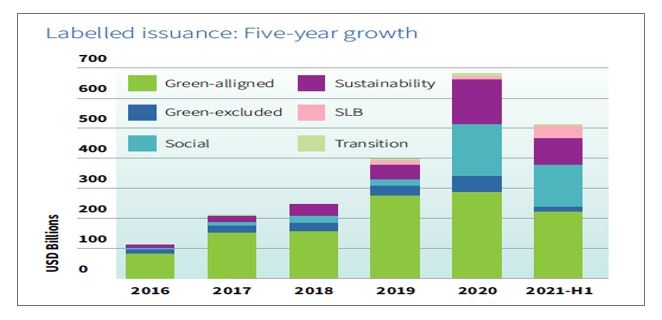

According to the CBI, total sustainable debt issuance increased 60% year-on-year between 2020 and 2021 and doubled between 2019 and 2020. Green bond issuances doubled in H1 2021 versus the same period in 2020 and is projected to surpass $500 billion in total issuance for full year 2021.

Source: Climate Bond Initiative

Noteworthy recent market developments include the largest corporate green bond issued by US retail giant Walmart in September 2021, a $2 billion green bond priced at 50bps over UST which tightened from 75bps over UST and priced well inside Walmart’s comparable plain vanilla corporate bond spreads. There has also been a proliferation of sustainability linked bonds (SLB) over the last few years.

Enel, the Italian power utility company, issued the first SLB in 2019: a $1.5 billion SLB which was 3 times oversubscribed and priced 10bps inside comparable coupon pricing for Enel. The Enel SLB had a sustainability covenant that Enel achieve 50% renewables share of its power generation portfolio by the end of 2021 failing which investors receive an additional 25bps increase in the bond spread.

Source: Climate Bond Initiative

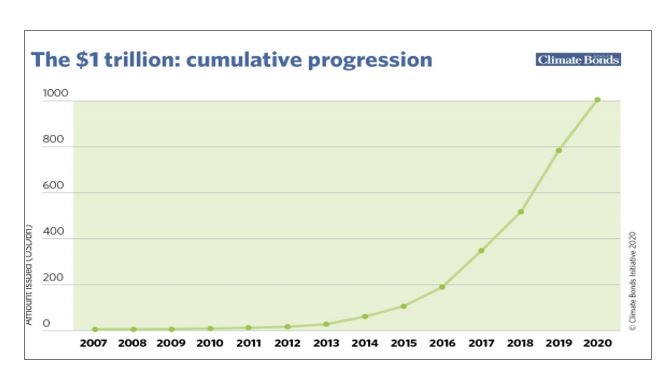

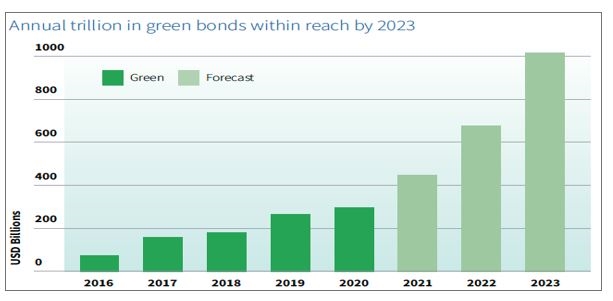

By the end of 2020 total cumulative green bond issuances reached $1 trillion. According to the CBI, annual green bond issuance is projected to reach $1 trillion by 2023 at the current rate of annual growth.

Source: Climate Bond Initiative

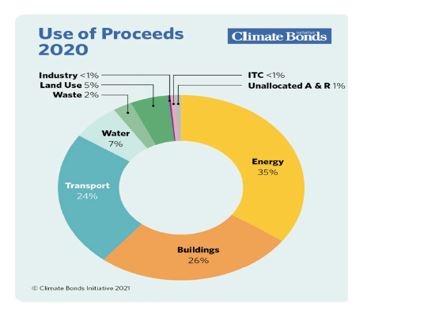

In terms of use of proceeds, buildings, energy, and transport represented about 80% of green bonds in 2020.

Green Bond Fund Case Study – The IFC-Amundi AF-EGO Fund

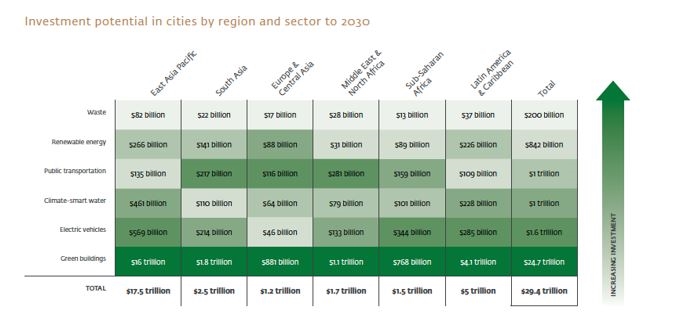

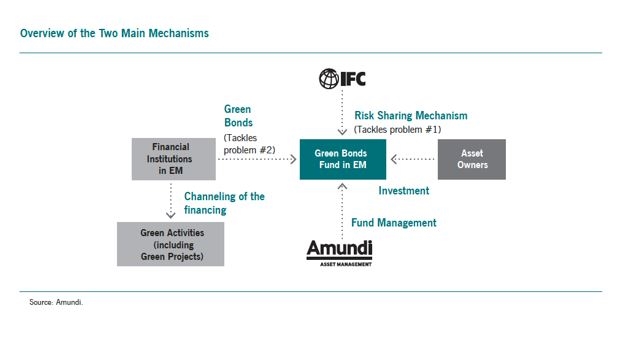

One of the most exciting and innovative game changer developments to create a marketplace for green bond investors and issuers alike has been the global green bond launched in March 2018 by the IFC and European fund manager, Amundi. The IFC projects that by 2050, 70% (6.7 billion) of the global population will reside in cities. The IFC identified the scale of climate change mitigation and adaption investment potential in emerging markets cities across 6 urban sectors out to 2030 at almost $30 trillion[i]. The challenge was how to devise a new funding paradigm which stimulated demand side green bond investment as well as green bond issuance supply at scale with acceptable risk adjusted returns.

Source: IFC

The Amundi Planet Emerging Green One (AP-EGO) fund with a target size of up to $2 billion of institutional capital to deploy, is the largest green bond fund in the world targeted at emerging markets green bonds. The IFC provided the initial seed investment of $256 million which catalyzed $1.4 billion of private sector capital investment from global pension funds, insurance companies and international development banks, thus achieving a 16x multiplier factor. The AP-EGO fund will subscribe a maximum of 5% of any given green bond issue, as such the fund provides a basis to catalyze up to $40 billion of potential investment. It will initially invest in a mix of green and non-green bonds (sovereign, quasi sovereign and other bonds issued by financial institutions) with a 7 year time investment horizon to transition to 100% green bonds given the current dearth of emerging market green bonds. AP-EGO will be a 100% green bond fund after 7 years as the green bond issuance market grows.

The fund is a structured, layered green bond fund with a credit enhancement feature provided by the IFC – and underpinned by its AAA credit rating - to mitigate certain investor risks. This is achieved by originating and including a diversified portfolio of green bonds in the fund with an IFC funded first loss tranche to improve the overall credit risk profile and achieve a target investment grade/high quality sub-investment grade credit rating[i]. The senior fund tranche represented 90% of the fund’s portfolio with the first loss junior (6.25%) and mezzanine (3.75%) tranches representing 10% of the investment portfolio. The fund is essentially a collateralized green bond structured fund with an imbedded securitization feature which allows AP-EGO to list the investment grade senior fund tranche shares, thereby facilitating secondary market trading liquidity, which is critical to meeting certain investor’s bond trading requirements. The fund is groundbreaking in that it seeks to address 2 fundamental problems which have plagued financiers looking to scale up emerging markets infrastructure investments; firstly, how to mitigate emerging markets sovereign credit risk and secondly how to originate sufficient emerging markets green bonds to meet developed market institutional investor’s needs.

The aim of the fund is to create a paradigm shift aimed at removing the current institutionalized barriers to the flow of sustainable infrastructure investment at scale from developed market investor capital to emerging markets, and in doing so, usher in a new infrastructure asset class.

Fund Performance – 31 October 2021

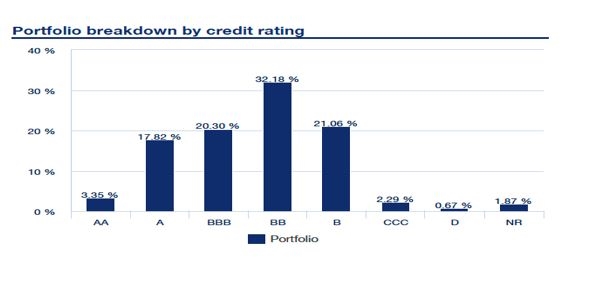

As of October 2021, the fund had $1.5 billion assets under management with 55% of the portfolio invested in private sector emerging markets green bonds across 85 issuers. The average credit rating of the fund was BB+ with return yields – particularly for the junior tranche – outperforming investor expectations.

Conclusion

Green bonds and the AP-EGO green bond fund represent a potential game-changer in the drive for greater financial innovation to help unlock and direct the $1.3 trillion of available institutional capital towards infrastructure investment. That said, it does have some limiting factors which may reduce the application to pan emerging markets, including the need for eligible emerging markets to have sovereign credit ratings – currently only 50% of countries in the Climate Vulnerable Forum have sovereign bond ratings. Other challenges include further streamlining the project identification and selection process and the post facto testing of the sufficiency of the 10% first loss tranche.

Citations

[1] IFC, “Climate Investment Opportunities in Cities – An IFC Analysis” (2018)

[1] Journal of Applied Corporate Finance, “Global Public-Private Partnerships: A Financing Innovation with Positive Social Impact”( Patrick Bolton, Columbia University, Xavier Musca, Crédit Agricole Group, and Frédéric Samama, Amundi Asset Management, Spring 2020)

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.