DigitalBridge – the digital infra pioneer

Digital infrastructure (DI) as an asset class has benefited in recent times from strong secular tailwinds around connectivity and the growing importance of access to data, which in turn is driving an upsurge in activity in this space.

- A version of this story appeared in The Global Digital Infrastructure Survey 2021 and associated report

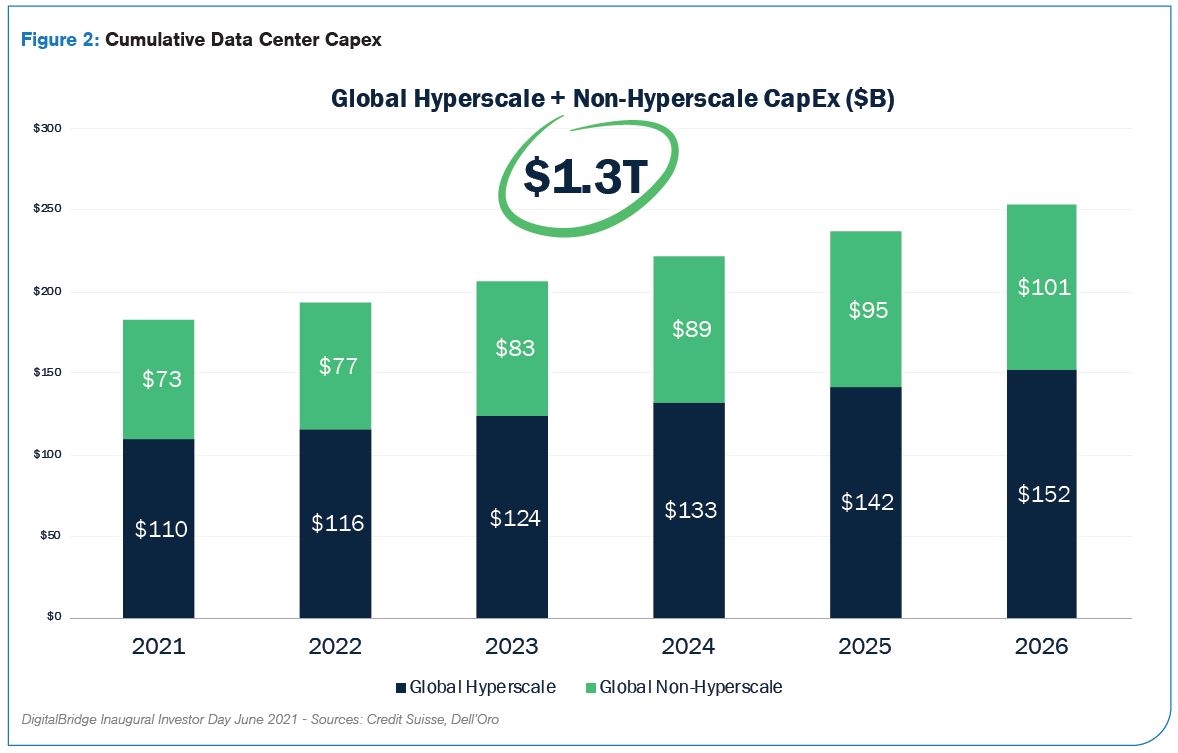

As it stands, there is a requirement for $1.1 trillion of worldwide investment in mobile capex with about 80% of that sum being deployed on 5G buildouts. This headline figure, however, is likely to be overshadowed by the global data centre capacity buildout.

These investments are key as Internet of Things (IoT) devices impact the market on a daily basis and telecom networks are re-framed and proliferated, making it all the more important for the DI community to fully understand challenges faced on a global scale.

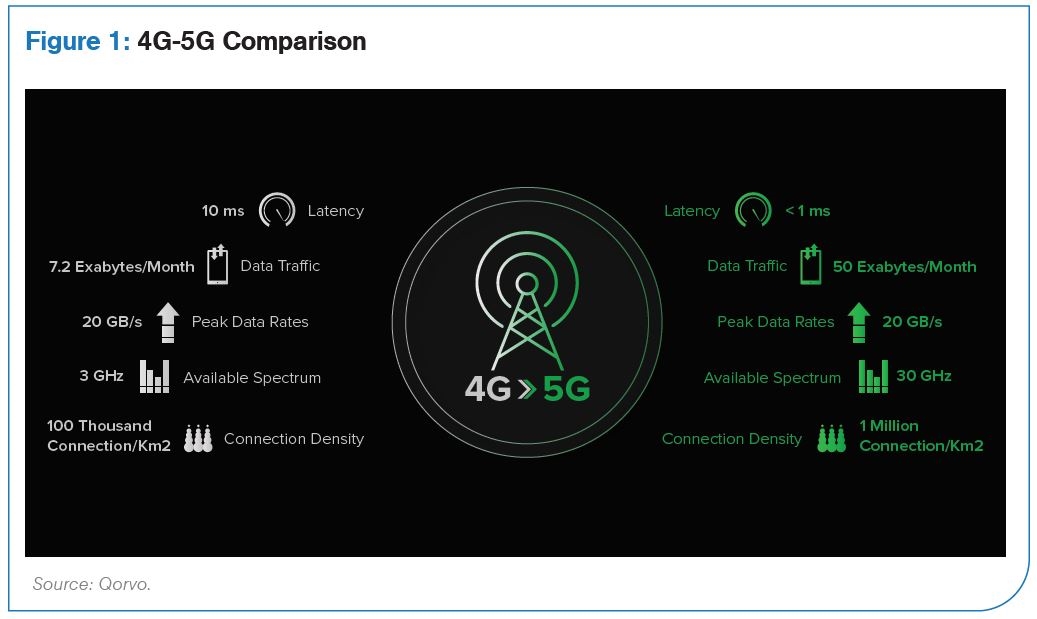

The movement to 5G – a predictable transition that occurs every 7-8 years as mobile technology evolves to the next level – will bring about a step-change in mobility as the market goes through one of the biggest radio technology changes ever seen (Figure 1: 4G-5G Comparison).

Meanwhile on the Cloud side of the DI spectrum, migration is moving at pace. Ten years ago, less than 1% of data were hosted on the public cloud. This rose to 18% last year (2020) with full-year stats for 2021 expected to mark a significant increase, aided in no little part by the Covid-19

pandemic.

For organisations like DigitalBridge that are entirely focused on this ecosystem, track record is all important, and with 27 years’ investing experience in the DI space, no asset manager is better placed to give its views on the market.

Here Marc Ganzi – CEO of DigitalBridge – explores the global opportunity afforded by the upsurge in investments across the international DI arena, identifying key trends over the next 5-10 years while also sharing a cautionary tale.

DigitalBridge

Timing of the publication of the Global Digital Infrastructure Survey 2021 and this report (its second iteration) is ideal given that the DI sector has witnessed a surge in activity over the course of the last two quarters with asset allocators rushing into the space where DigitalBridge is a leading REIT.

DigitalBridge is the only dedicated, global-scale DI firm investing across the ecosystem in towers, data centres, small cells, fibre, and the emerging Edge infrastructure vertical – ideally placing it as a thought leader in this burgeoning market.

DigitalBridge manages more than $35 billion in assets focused exclusively on the DI opportunity. And this impressive set of assets under management (AUM) has increased by more than 70% since Marc became chief executive last year (2020).

The last few months have been especially active for DigitalBridge, having announced in July the formation of EdgePoint Infrastructure, a leading wireless tower platform in Asia. This investment

was preceded in June with completion of the acquisition of Boingo Wireless – a US distributed antenna system and Wi-Fi provider that serves carriers, consumers, property owners and advertisers globally.

In May, DigitalBridge also celebrated the launch of AtlasEdge, a joint venture with Liberty Global to develop Edge data centres across Europe.

One of the key differentiators between DigitalBridge and other asset managers is that it has unique capability to invest, operate and build digital infrastructure. It has the investment experience of an asset manager, deploying capital on behalf of (and in partnership with) large institutional investors that are attracted to the growing, but resilient profile of DI assets.

Market Demand

In recent research, IJGlobal identified cash raised in H1 2021 by unlisted infrastructure funds to target activity in the telecom sector accounted to 12% of all funds to reach final close in that period. As to M&A activity, it is outpacing funds raised in a sector that is not solely reliant on infra funds.

However, the market-wide upsurge in fundraising and M&A activity will play a key role in achieving digital transformation – the integration of digital technology into all areas affecting industries, businesses and consumers, fundamentally changing how the market operates and delivers value to customers.

This transition is set to increase as IDC in a recent white paper predicts that by 2025 nearly 30% of data generated will be realtime, driven by both consumer preference and enterprise needs for real-time data.

The need to invest will continue to drive greenfield developments and – every bit as important – M&A activity as players seek to consolidate their positions.

“The rush by asset allocators is entirely predictable,” says Marc. “This sector has attracted so much attention because GPs can write huge cheques in this space.”

Marc adds: “Some infrastructure asset classes are out of favour these days – like mid-stream energy due to ESG policies – and investors are looking to find the next big thing… and digital infrastructure is at the top of every infrastructure GP’s agenda today.

“That alone adds a whole new layer of complexity because you have a ton of capital flooding into this space with people who do not have an industry operating background, while bankers peddle deals indiscriminately.

“We are at a great take-a-step-back moment to stop and define what is ‘digital infrastructure.’ It is essential that we be intellectually honest about it and define what makes it infrastructure and what makes it not infrastructure.”

Given DigitalBridge’s experience in the DI market and its international scope, it opens up a great deal of opportunity for this market leader to cherry pick its targets.

“We are spending our activities in multiple geographies and sectors,” says Marc. “We take a very customer-centric approach to how we put capital to work – and that is obviously going to differentiate us from our peers.”

DigitalBridge takes an thoughtful approach to targeting markets and sectors for investment, building on the team’s experience and understanding of how digital infrastructure is evolving.

“There are four big thematic microtrends below the secular trend of digital infrastructure,” says Marc. “Take a look at big asset allocators. Many of them are super focused on digital because they are telegraphing to The Street that they are secular investors, investing in a secular trend

that they think is big… and digital is top of the list.

“But you have to ask what is their investment thesis? Where are you going and what is driving their approach?”

Marc continues: “What we say to investors is that over the next decade there will be four things that will change our lives and that will profoundly change in themselves… and these are: Cloud adoption; the usage and proliferation of IoT devices; the movement from 4G to 5G; and then the movement towards the Edge.”

“With the Edge, you have to consider where servers are going, where the capacity is required and where is the computer workload heading,” says Marc. “One of the great secular trends coming out of Covid is this migration to digital – all things digital – and this is what has allocators rushing into the game.

“We are building large cloud campuses across Europe, Latin America, North America and Asia – and we think the ability to service cloud customers around the globe is an important macro trend.”

Global asset allocater

DigitalBridge’s union with Liberty Global (one of the world’s leading converged video, broadband and communications companies) is an ideal case study for its strategy to create a joint venture –

AtlasEdge Data Centres – to serve growing European demand for scalable data centre capacity that brings applications and content closer to the Edge.

The JV is subject to receipt of customary regulatory and merger control approvals, and it is anticipated that the transaction will close in Q3 2021.

When it comes to partnering on such landmark deals, it is essential that both parties are skilled in the digital infrastructure space.

“We have a team that’s been doing this for more than 25 years, with deep industry relationships that drive access to proprietary investments and position us to continue to be a leader in digital infrastructure,” says Marc.

“We are very focused on Edge computing in Europe and we think the proliferation of Edge servers in pushing workloads out to the perimeter of the network in Europe is a big trend.

DigitalBridge has a strong focus on towers and has built impressive footprint in this space.

Marc says: “We made a significant investment in Vodafone’s tower business, Vantage Towers. Why? Because we believe it is a fantastic business and Vodafone is a great and long-standing customer of ours. Vodafone requires a significant amount of capex to deploy for its 5G infrastructure. That is a great example of investing in the future and investing in 5G.”

On the Cloud side of the business and the migration to Cloud, DigitalBridge has clearly identified Asia as a key market for investment.

“Asia is a unique market and we formed a business there called AgileDC which is building large web-scale campuses throughout the region,” says Marc. “The starting point there has been in Japan, but we continue to target South Korea, Australia and Singapore as key markets for greenfield development. We also recently announced the acquisition of PCCW’s assets in Hong Kong and Malaysia which will accelerate our scale in the region.”

“All of the major cloud players need to build more infrastructure in Asia and we believe this is going to be one of the great opportunities in the digital infrastructure space.”

The Internet of Things (IoT) ranks as a primary opportunity for DigitalBridge.

“Thinking through the future of wireless networks and all things related to IoT, we made a significant investment in Boingo which is one of the largest owners and operator of indoor wireless networks and Wi-Fi networks,” says Marc.

“Those Wi-Fi networks support Enterprise 5G but also support the proliferation of IoT devices inside key venues like airports and stadiums, office buildings and hotels where you can deploy next generation technologies based on Wi-Fi 6 which will ultimately help to manage facilities. It’s more than just mobility, it really goes to the operation of the enterprise.”

DigitalBridge is taking a sector-wide approach to the market… on a global basis.

“We are working in 5G, Edge, towers and Cloud and we have four case studies from the last six months into why we are investing and how we are investing,” says Marc.

“What is interesting is that we’re doing this in the US, Latin America, Asia and Europe… these trends are global in nature. One of the great things about digital is that it transcends boundaries and we have done a great job of demonstrating that.

“We are super busy. We have a lot happening. But we’re going to stay true to these thematics and continue to invest on a global scale.”

A cautionary tale

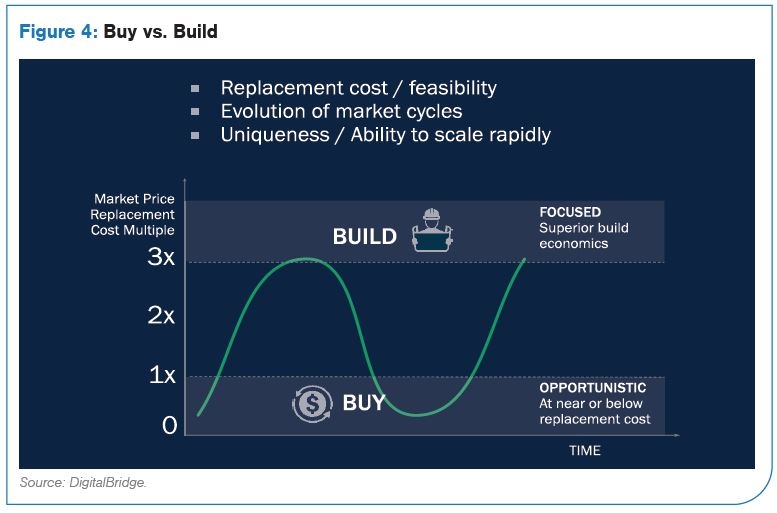

Any market observer worth their salt will have taken note of a frothy digital infrastructure market which should set alarm bells ringing as prices sky-rocket and competition leads those with less experience to make bad decisions… particularly in an environment where competition can scale up swiftly (Figure 4: Buy vs. Build).

“A cautionary tale… there’s always an in-favour asset class, so you have to be aware of the risks. Take a look at midstream energy which was the darling of infrastructure 6-7 years ago – and look what happened.

“You saw a lot of marginal management teams moving into the space, raising a lot of capital and feeling the pressure to deploy. This is a conundrum for GPs today – they are on this constant journey to raise more and more money, launch fund after fund, and get fees… but you have to operate the assets.

“Operating the assets is hard. This is not a utility, an airport or a toll road. These businesses are complex and require a deep understanding of technology, your customers, their needs, and the migration path of that network.

“And that’s not easy.”

DigitalBridge has the benefit of experience having been working in this space for more than 27 years and – up until a couple of years ago – forging its path pretty much alone. That environment has changed dramatically in recent years.

“Now everyone else wants to do it,” says Marc. “But my counsel to investors is – do your homework and make sure there’s a strong operating team running these assets as it’s a hard and complicated business.”

With the prices that assets are currently fetching in a frothy market achieving eyewatering multiples, caution should be every investor’s watchword.

“We see an alarming trend between the dislocation between M&A prices and ultimately the replacement cost of new facilities. One of the things you can do in this business is over-build,” says Marc.

“While it’s very difficult to build a new water system or an electricity transmission grid for an entire city, those deals have huge barriers to entry and they trade for the appropriate multiples.

“With businesses in the digital infrastructure space, you can build other fibre networks, data centres, you can overbuild or put another cell tower next to an existing cell tower.”

Marc adds: “The ability to build on a greenfield basis is hard and that requires a set of skills that infrastructure GPs generally just don’t have.

“So this is going to be a really interesting 5-10 years in investing because the teams that really understand the operational complexity of these assets are going to do well. Meanwhile the teams that do not have that understanding of the operational complexities are not going to do quite so well.

“We are moving into a very bubbly top of the market type of environment and this is where we need to be careful. We need to be prudent, disciplined and this is a moment for pause and reflection. Yes, these are amazing secular trends, but there are also some things happening that are a bit unnatural… purely from a returns perspective.

“Our firm is being very disciplined right now. Discipline is our battle cry at DigitalBridge.

“We have made it here for 27 years and my hope is that we are here for another 27… and the only way we’re going to manage that is if we are disciplined allocators of other people’s capital.

“That is our job – to be a great fiduciary.”

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.