Mitigating risk shock in European wind

Investors and utilities in the European wind sector face increasing headwinds from political, regulatory, social and lifecycle risks as support schemes end, according to William Cox and Mathew Garver of M&E Global, Inc.

The rub lies in whether calculation on funds needed and cash flows expected for a wind project do not consider key risks, such as political, regulatory and lifecycle, and – as a result – expected returns may soon turn red.

A new government seeking public support, an added retroactive tax, a change in regulations, a legal battle or administrative backup with regulators can mangle projected returns from wind projects.

And with unpredictable political winds blowing throughout Europe, such renewable energy projects can tip into unprofitability at any time.

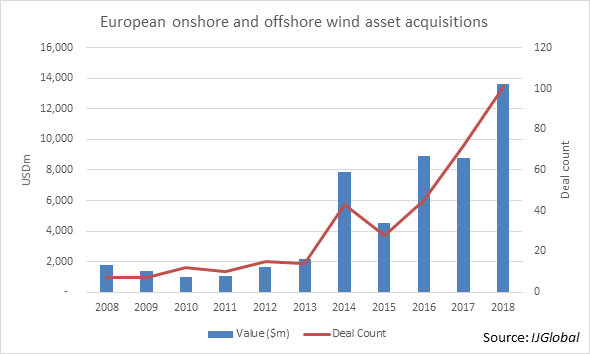

Drop in investments for new assets

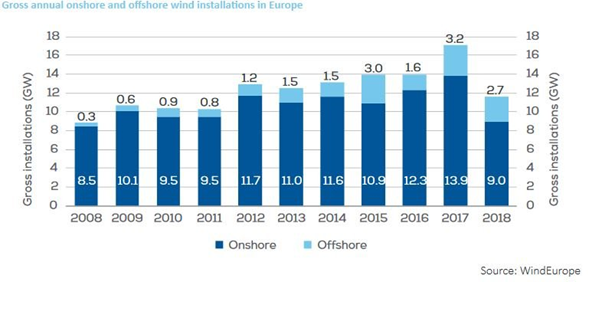

This "risk shock" led to a drop in investment and construction activity of new assets across the last two full years (2017 and 2018). In fact, 2018 was the weakest year for new wind installations since 2011. Onshore wind installations in Germany fell by half and collapsed in the UK.

Twelve EU countries failed to install any wind turbines in 2018. "The outlook for new investments is uncertain," comments Giles Dickenson, CEO of WindEurope in a recent report on the sector.

"In many important EU markets there are currently no wind investments, despite these countries having significant potential for further expansion of wind power. National energy policies and lack of a stable regulatory environment have affected both the level of investment and financial commitments in half of EU Member States."

Investors have identified existing assets as less risky, despite their likely need for technological upgrades. But technology investments are predictable and thus can be planned.

The subsidized growth story

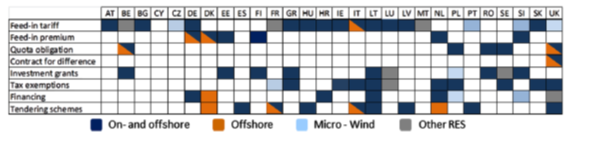

The growing installation of wind farms across Western Europe has been driven by its increasing maturity alongside a mixture of support measures, including guaranteed feed in tariffs and premium schemes, tax exemptions, financing, quotas, and tendering – in addition to various nation-specific incentive schemes.

In 2018, €65 billion was invested in European onshore and offshore wind energy – more than 60% of all energy investments in the region, and €26.7 billion was allocated to new assets.

Low interest rates and liquidity in search of investment were among the key drivers as 90% of new assets were financed with debt – the highest amount thus far.

Fitch Ratings forecasts that by 2026, some 27% of the primary West European energy mix will come from renewable sources. The European Union even raised its state-wide binding target to 32% by 2030.

Utilities are investing heavily, supported by external investors. For example, in the first nine months of 2018 Iberdrola committed 34% of its net investment to renewables, its second largest investment area.

Risk shock as subsidies fall away

However, under the surface, not all is well. The European wind sector is currently undergoing one of the most significant transitions in its 20 year history. As government subsidy and support schemes fall away, it is becoming exposed to a host of risks which, thus far, it did not have to worry about.

Until 2016, incentives and guaranteed FITs allowed investors and operators to enjoy fairly predictable cash flows and margins from wind farms. The major risk areas lay in design, technology and construction.

Until recently, roughly 75% of Europe´s wind energy capacity was protected against market risks by some form of subsidy or support scheme. By 2030, only 6% will be "fully protected", leaving 67% of Europe´s wind capacity partially-exposed, and 27% fully-exposed to market risks, according to SwissRe.

In addition to dropping incentive schemes, projects have been auctioned to the lowest bidder, depressing prices by 50-80% between 2015 and 2018. Auctioning also meant that developers would no longer be guaranteed a minimum electricity price.

Developers now see themselves in a whole new game where they are exposed to a host of new risks, including price (merchant) risk. One study shows that merchant risk could be 2-4x greater than construction risk. For example, an increase in risk premiums of 150 to 250 basis points translates into additional 20-30% in Capex. (Anand Gupta: 2018)

Developers are reacting by trying to lock in FITs and Feed-in Premiums (FiPs) via power purchase agreements (PPAs), which are attempts to at least control price risk.

"We continue to focus... on the execution of our organic growth, securing long-term contracts," Antonio Mexia, chief executive of EDPR, said at a Q3 2018 earnings presentation.

"EDP Renewables has currently secured 3.4GW of PPAs and feed-in tariffs for new wind and solar capacity to be commissioned over the next years," he added, citing contracts signed in the US, Europe, Canada and Brazil.

However, price risk is only a part of the story. Increased exposure to merchant risk has driven developers to seek economies of scale in ever larger wind parks. While new asset investments in 2018 were below 2016 levels, the total GW financed was considerably higher (16.7GW in 2018 compared with 10.3 in 2016).

Political risks go up – tech risks go down

Perhaps the biggest risk category is political and regulatory alongside higher lifecycle risks.

Political risk centres on the likelihood of legislative branches passing new laws, and regulatory is the risk of these laws and guidelines generating regulations which make the success of cash flows and profits from wind operations less certain.

The reason these risks are perhaps the most venomous is because politicians and regulators can change their minds and regulations at any time irrespective of guidelines thus far in place.

These changes impact most contracts from a macro-economic level, thus upsetting any cash flow calculation radically. Furthermore, political decisions tend to be far-reaching and their full financial implications hard to anticipate.

New taxes are a prime example:

- some municipalities in Belgium started to levy an additional fee for existing and new wind turbines mid-2012

- Romania suddenly introduced a 1.5% construction tax on tangible assets

- Greece in 2012 introduced additional taxes on the gross income of all operating RES operations

- France’s IFER tax is levied on all electricity producers, but wind plants pay a higher rate

- the Polish government is being sued by US developer Invenergy for $700 million in losses due to what they claim to be akin to an expropriation

- in Bulgaria, since May 2012, connection to the grid of renewable plants with a preliminary grid connection contract was pushed to 2016. And, since mid-March 2014, distribution system companies have been limiting the maximum power generation of all wind and photovoltaic power plants by 60% (European Commission: 2015)

A study by the EU outlines Romania´s drastic retroactive policy changes: "Romania introduced in 2013 retroactive regulatory changes that fundamentally changed the economics for existing installations.

"Mandatory acquisition quotas for green certificates – which were defined by law till 2020 – were slashed drastically (in 2014, the quota reductions were over 25%, as the obligation was reduced from 15% to 11.1%); energy-intensive companies where exempted largely without redistribution of the obligations; the validity of green certificates was reduced from 16 months to 12 months; the envisaged implementation of the guaranty fund, that should have bought excess green certificates, was repealed.

“All these measures resulted in green certificate prices being cut by half and caused extreme oversupply which may result in many green certificates to expire and therefore be worthless.

“Furthermore, half of the green certificates produced between 2013 and 2017 were delayed to the period of 2018 and 2020, which causes financial losses even if a recovery would be possible.

“Green certificates are not granted anymore for electricity produced above the physical notifications of the day-ahead forecast. New priority dispatch of certain national coal generation and changes to balancing market rules led to additional, non-remunerated, production curtailment."

Political and regulatory risk is cited as the major reason for low investment in South Eastern European countries, where total investments are only €1 billion, or 4% of the total European investments in new wind assets in 2018.

A part of regulatory risk is administrative risk, such as that in Germany. New onshore wind farms in Germany are de facto being stopped by a slow permit granting process. It used to take 10 months to secure a permit for a new wind farm. Now the process takes more than two years. Not a single onshore wind turbine was ordered in Germany in Q1 2019.

Full risks neither considered nor mitigated

The worrying element is that these risks are not being priced into the cost of capital.

Average interest rates charged mainly by the 67 banks providing debt to European wind projects have consistently fallen despite increases in merchant and other risks.

Interest rates only seem to reflect default risk as well as declining construction and completion risks as technologies mature.

The real risk for investors

The missing link is a method and process to calculate, manage and mitigate these very real risks to insure predictable cashflows and sufficient for financial provisions to hedge these greater risks.

This means defining an accurate cost of capital, which accurately prices political, regulatory and lifecycle risks.

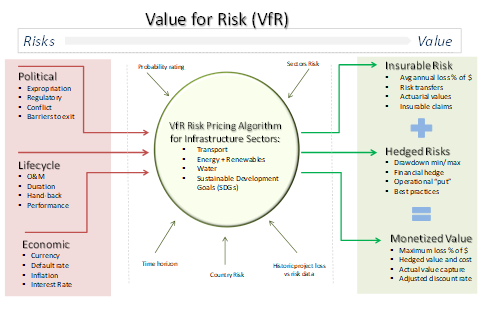

A method developed by M&E Global, Inc., the financial analysis boutique, in partnership with IJGlobal, called Value for Risk – VfR – calculates and helps mitigate hundreds of difficult-to-calculate risks in 3 categories:

- political risk (social risk, regulatory, governance, legal): social pressures by environmental or interest groups driving legislative changes, changing guidelines and bureaucracy as well as potential legal pitfalls

- lifecycle risk (O&M): maintenance and material fatigue risks, for example, can develop exponentially, impacting the entire risk profile of a project

- economic risk: interest rates, inflation, growth, national and sectoral ratings

VfR allows industry practitioners to define current and complete cost of capital by calculating each risk in terms of basis points. Risks are split into all sub-risks to identify where they originate and how to mitigate them – allowing the realistic discount of projected cash flows from the project and provision for risks.

Once risks are calculated, VfR indicates the best way to mitigate each risk. The below chart illustrates a VfR risk overview (not including technical risks), demonstrating how the cost of capital can be driven down in individual risk areas.

VfR does not calculate technical risks – such as construction, weather or production levels – but the VfR risks that have direct influence on pricing. Legislators are known to change laws at will, voiding key parts of contracts, as in the case of Spain in June 2014, when FITs were reduced to six years.

Value for Risk VfR Sample Risk Matrix for a given wind project*

|

Value for Risk (VfR) main Risk Categories |

Risks at in basis points (bps) |

Mitigation instrument |

Potential mitigation in bps in 5 years |

Mitigated risk in bps |

|

Base risk (cost of capital) |

170 |

Debt investment |

(0) |

170 |

|

Political, social risk |

65 |

Hedge |

(18) |

47 |

|

Regulatory, governance, process risk |

50 |

Optimizing internal processes & planning, incl. legal monitoring |

(20) |

30 |

|

Lifecycle, O&M risk |

58 |

Technical monitoring, maintenance, insurance |

(32) |

26 |

|

Financial, macroeconomic risk |

48 |

Hedge, PPA, FIT, FIP |

(35) |

13 |

|

Minus risk priced into Base risk |

(68) |

-- |

(68) |

(68) |

|

Total real Cost of Capital (without technical risks) |

323 |

|

(105) |

218 |

*Hypothetical data for demonstration purposes only. Source: M&E Global, Inc.

Importantly – although base risk is mainly focused on default risk – it may price in some countries, political and financial risk. Part of the VfR system is to estimate how much is priced in and subtract it from VfR risk totals to avoid double counting. This part relies on estimates as bonds are blunt instruments that do not actually (or accurately) price risks. They price market demand for debt.

Importantly, risks change over the lifetime of a project as much as political legislation, policies and economics fluctuate. Thus, VfR functions as a lifecycle risk mitigation tool.

VfR does not use a scenario approach, as is frequently applied to technical risks in wind. Scenario approaches are useful for technical risks because the number and profiles of potential outcomes are limited and fairly predictable.

The VfR method analyzes structures, functions to determine what could go wrong in combination with statistical analysis of historic data on what has gone wrong. These two data sets are merged into a proprietary algorithm and translated into basis points. The VfR risk is dynamic and adjusts real time to changing realities impacting a project.

Knowing your risk exposure is key both to pricing returns from debt and equity. Power producers hold roughly 60% of wind equity with financial investors making up nearly 40% and corporates at 3%+ in Europe.

Financial investors are warming up to the idea of holding equity throughout the operations phase, which creates a particular exposure to risk. This risk can be actively controlled using VfR.

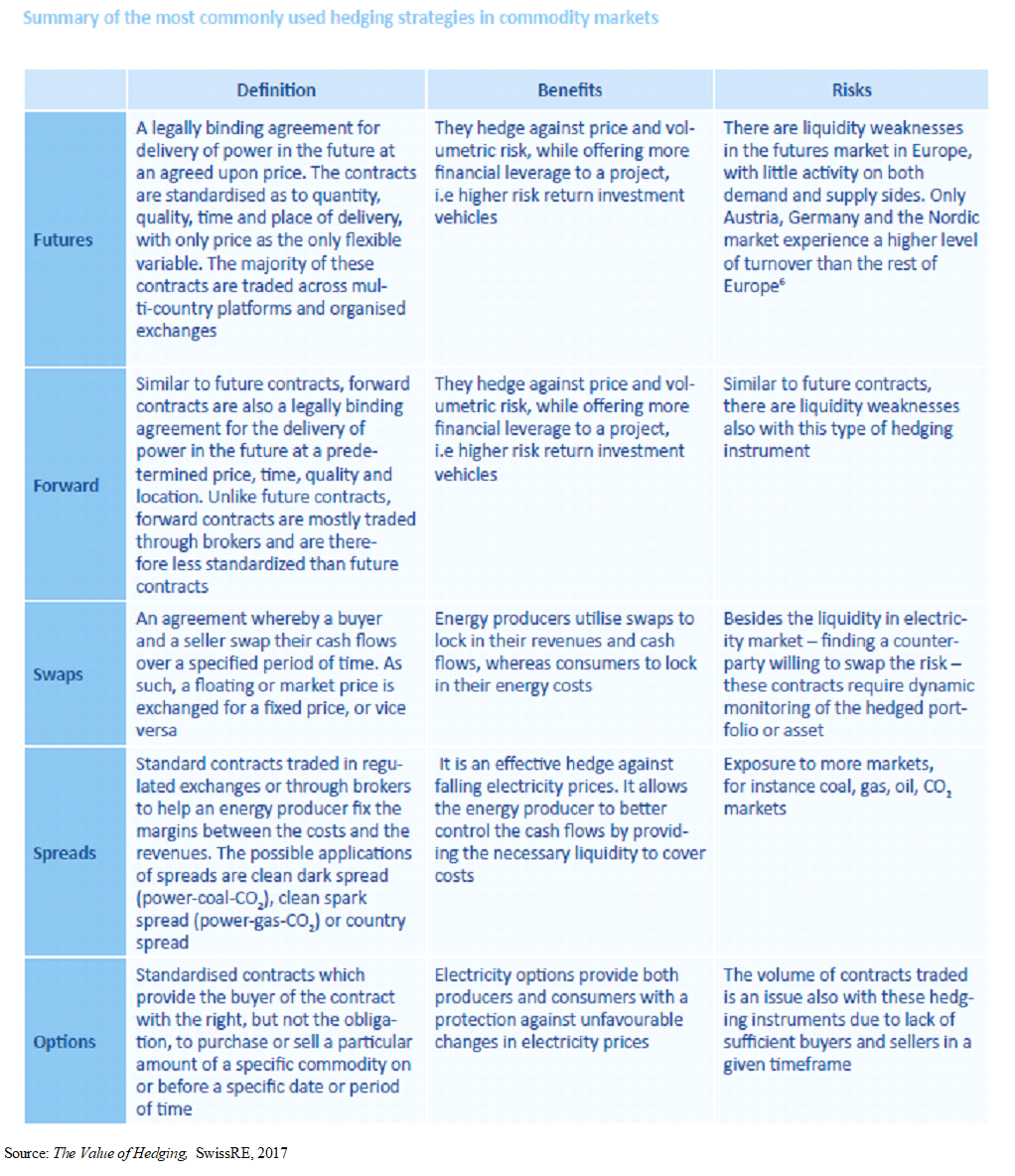

VfR prices relevant risks, allowing practitioners to construct hedges of different kinds (see chart below).

Stuart Brown, head of origination weather and energy APEMEA, says: "Volume hedges for wind have been available for several years, but the take-up has been limited because they weren't needed.

“But as merchant risk becomes more dominant, the value added by hedging production may come to be make-or-break for greenfield, re-structuring and PPA wind development."

As hedging gains popularity in the wind sector, SwissRE estimates that hedging could generate an added €7.6 billion in value which would flow into new wind assets between 2017 and 2030.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.