LT analysis: Bond rush

IJGlobal's full-year league table data shows the total value for energy and infrastructure bond financings in 2015 reached record levels, with the majority of issuance for North American assets.

In the 12-month period to 31 December 2015, a total of $28.8 billion of energy and infrastructure bonds reached financial close, up from $26.8 billion in 2014 and $27.8 billion in 2013. Of that total, over half - $14.6 billion - was connected to US-based assets, up from $9 billion during the previous year. There was a total of 90 project finance bonds closed globally during the year, compared to 73 in 2014.

Developers of North American projects have long been able to raise debt in the bond markets more easily than sponsors in other regions, with domestic investors more comfortable with infrastructure as an asset class. The total volume of bond financings in Europe has only surpassed the North American total for one year (2013) out of the last eight.

The difference in total bond financing volumes between these two markets was probably so pronounced in 2015, and the North American total so high, because of the impending interest rate rise from the US Federal Reserve. Lower interest rates since 2008 have encouraged corporate bond issuance. The rise in the fed rate from 0.25% to 0.5% in December was widely anticipated, and many issuers will have tried to close bonds before the end of the year. While bond activity grew in Europe in 2015, the competitiveness of its local bank market, and consequently the relative cheapness of bank debt, meant it did not grow as fast as in North America.

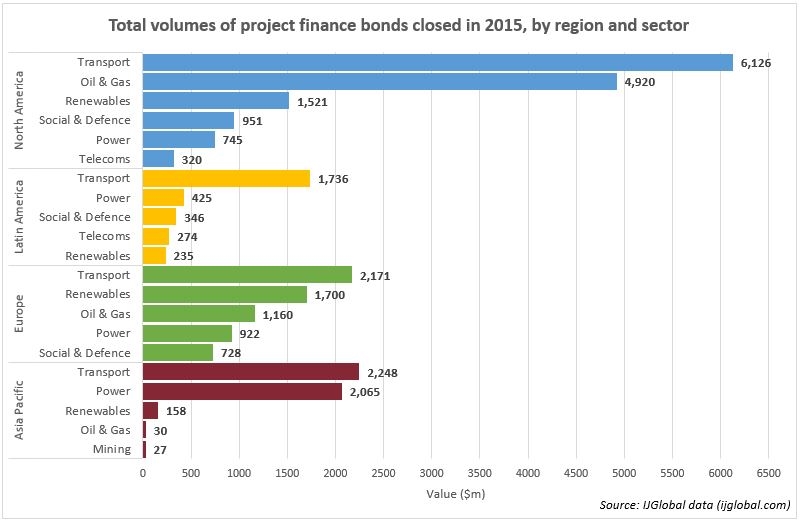

Bond issuance for energy and infrastructure projects rose in North America, Europe and Asia Pacific in 2015 compared to the previous year, but fell in Latin America and was non-existent in Africa and the Middle East.

Bonds are typically only raised in the Middle East against large capital intensive projects, typically in the oil and gas and power sectors. These deals tend to also tap local and international bank debt. A number of large projects in the oil and gas space were delayed or cancelled last year due to depressed oil prices, while the only significant power project, Facility D in Qatar, featured only bank debt and failed to reach financial close before the end of the year.

A breakdown of sectors shows that bond financings matched wider trends in the energy and infrastructure space, with renewables and transport volumes growing while the issuance of power and oil and gas bonds declined.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.