A project bond refinancing boom, when rates rise

Europe should continue to see a high number of projects refinanced in 2016, even if the recent interest rate rise in the US is followed by similar moves in the UK and continental Europe. But a reduction in breakage costs for interest rate swaps may encourage debt raisers to opt for a capital markets option instead of bank debt.

Fed rate rise

On 16 December 2015, the US Federal Reserve increased its base interest rate for the time since 2006, from 0.25% to 0.5%. The move is viewed as the starting point for incremental rises over the next 12 to 18 months. Financiers have been speculating that the UK may follow suit, even if the Europe Central is likely to be slower to raise its rate.

The latest predictions are that the Bank of England in late 2016, or even 2017, will raise the interest rate from the 0.5% level it has been at since 2009.

Liquidity levels for both institutions and banks operating in the infrastructure sector have been high for the last year or so, and margins have been reduced as their costs of funding have kept low. As a result refinancing volumes in 2015 reached a volume unprecedented since 2005, according to IJGlobal data for European transport and social infrastructure, and 2016 is likely to offer more of the same.

Banks win out

Mike Wilkins, managing director for infrastructure finance at rating agency Standard & Poor’s (S&P), said: “Some project borrowers trying to refinance infrastructure deals in the capital markets over the past 12 months have hesitated at the last minute and have refinanced using banks.”

An S&P report entitled “Project Finance: rate rise may herald a wave of refinancing in the bond market” forecasts that the recently announced US Federal rate rise, and expected rises in the UK and potentially Europe, could make project bonds a more commonly selected option.

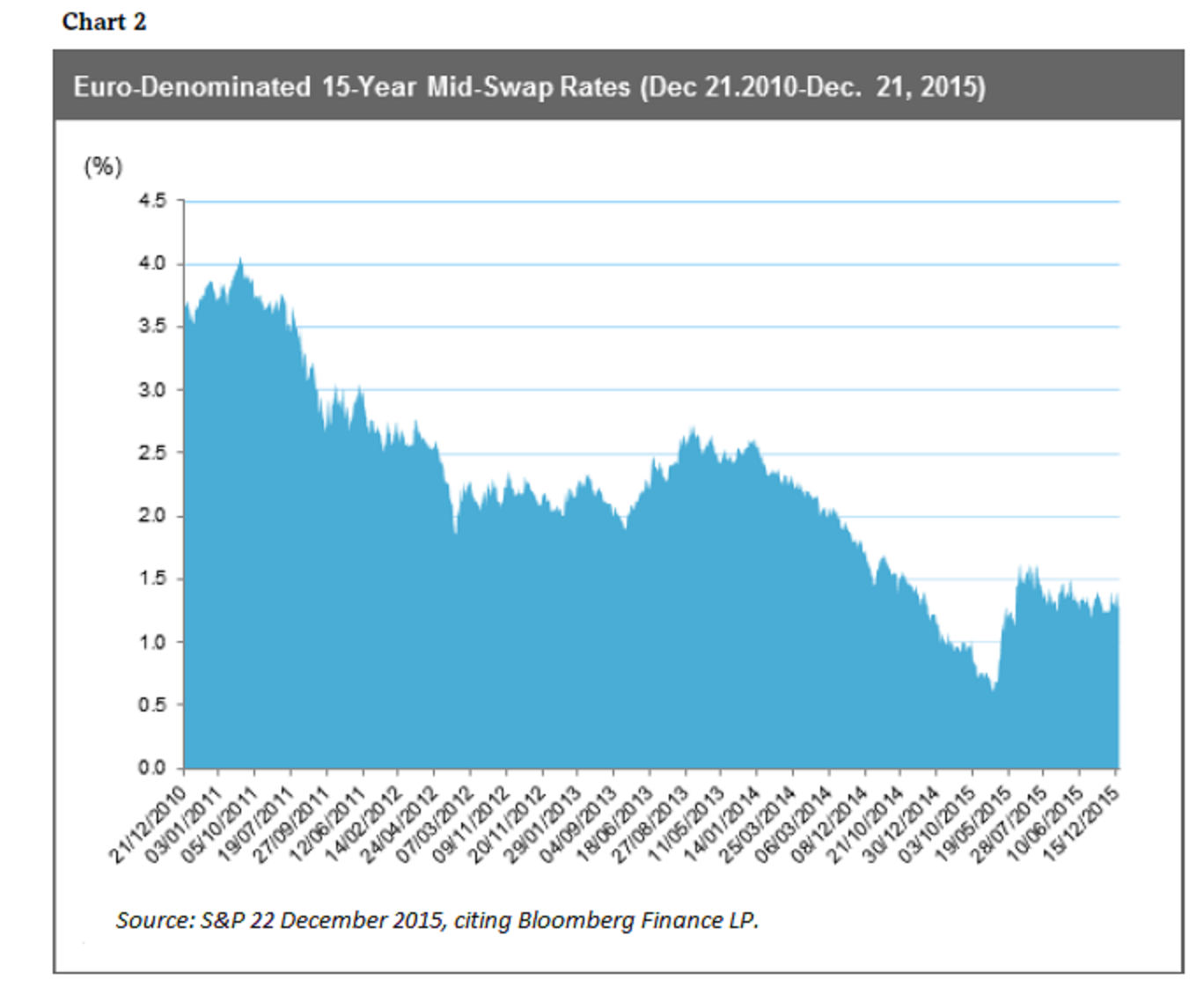

The reason: a rise in mid-swap rates commonly used to hedge interest rates for European project finance would reduce the swap breakage costs associated with moving to a bond financing.

The 15-year euro mid-swap rate at 1.3% in December is still near its historical low of 0.6% in April 2015.

That is far below the in the post-crisis 2008-2012 period. Projects closed in those earlier years did so with higher interest rate swap rates such as the 4% recorded in 2011. But they also had much higher margins compared to now, and so are natural candidates for refinancing.

Swap breakage cost deterrent

Costs resulting from breaking the original swaps that banks put in place are especially high when interest rates are as low as now. For example, if a deal had closed in 2008 at 5% underlying interest rate with a swap in place at that level, and the underlying rate is now 1%, for the borrower to unwind that swap they make a large mark-to-market payment, the foregone difference, to the swap provider.

Rishi Nihalani, head of infrastructure advisory at MUFG, said: “That cost normally comes out in the wash because [the borrower] effectively crystallises that foregone difference, but locks in at a new lower rate. In cash flow terms they’re broadly even but the problem is that, from an accounting point of view, it can impair their ability to distribute dividends and therefore yields.”

A large loss will flow through the borrower‘s profit and loss account, which can cause a restriction on dividend distribution despite cash being available and this may be very problematic.

Often the project bond has not been economical compared with a bank deal, for this reason.

Stewart Robinson, European head of project and structured bonds at Societe Generale Corporate & Investment Banking said: “Running both bond and bank processes in parallel is not unusual, and where the swap breakage cost is not too penalising, the bond solution can potentially present an equally, if not more, competitive offer than bank financing. Swap breakage cost is an issue for sponsors and comes up frequently when a project refinancing is considered. ”

On top of that hit, with low costs of funding the banks have been more than delighted to hold on to well-performing loans, and have used this and their visibility on deals to make competitive offers on their margin and covenants.

Lowering swap breakage costs

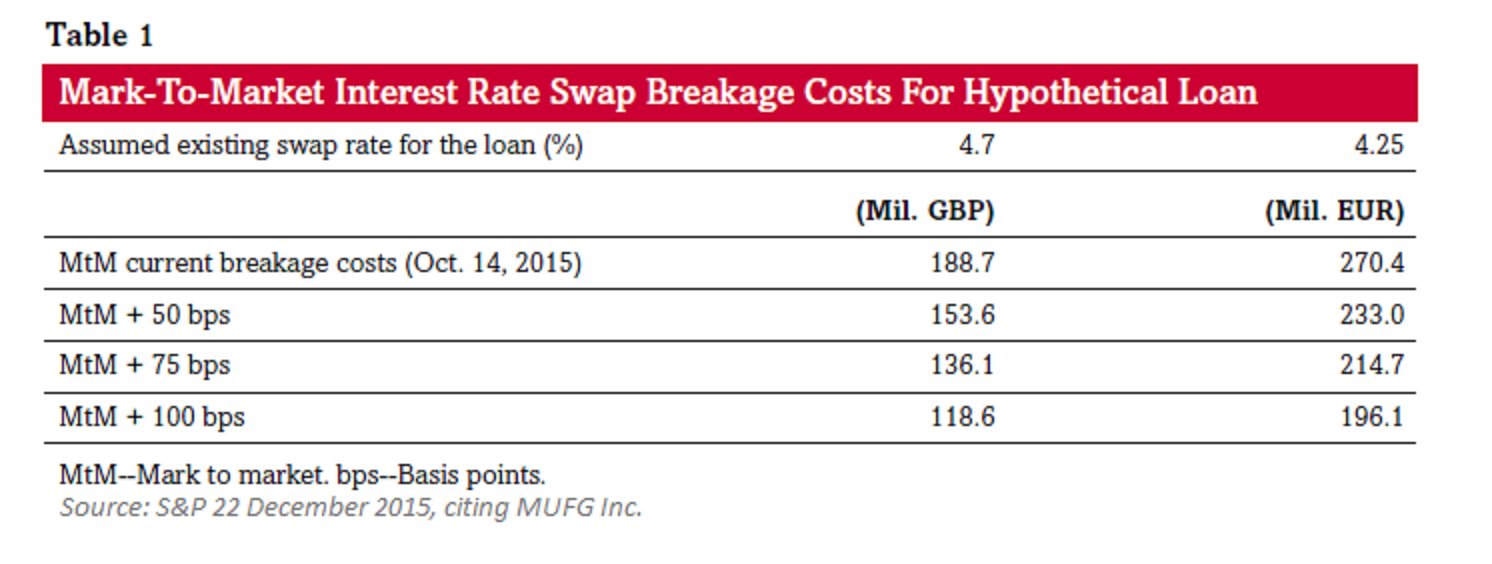

MUFG’s infrastructure advisory team and Mitsubishi UFJ Securities put together a simulation to illustrate the reduction to swap breakage costs, if the interest swap rate does rise. Based on an assumption of a 4.7% swap rate for a £550 million sterling loan closed in 2009, the mark-to-market breakage cost would reduce from £188.7 million (as at 14 October 2015), down to £153.6 million if mid-swap rates rose 50bp, or down to £118.6 million if they rose 100bp.

Wilkins said: “Long-term loans that were taken out immediately after the financial crisis, about 2008 to 2012, were put together at higher interest rates and now seem expensive to the borrower. There is a strong incentive to refinance as interest rates remain at a historical low, even if marginally increasing, and swap breakage costs will be coming down. There would be a sweet spot, from that confluence of all three elements coming together.”

Forecasting for 2016 might be premature. Robinson commented: “It is a considerable assumption that 2016 is the year that will see interest rates rise in the UK and Europe, however the effect of increasing rates on swap breakage costs is definitely something to consider for the next years.”

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.