The changing equity mix of offshore wind

The equity mix at pre-construction phase for project financed European offshore wind developments has changed vastly since the sector was born more than 15 years ago.

The first offshore wind farms were typical financed on the balance sheets of the utilities that conceived, built, and operated them. Now banks, private equity funds, pension funds, state-backed green banks and insurance companies have all been known to invest equity in these projects at an early stage.

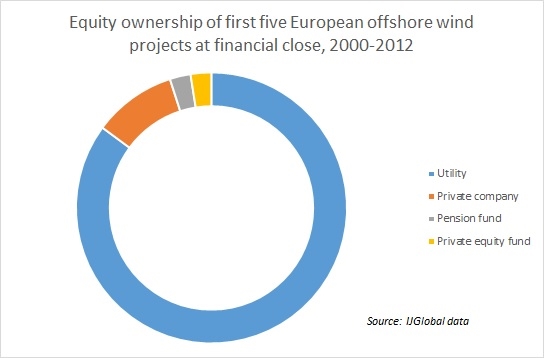

The first two financial close transactions for offshore wind on IJGlobal’s database - the 4MW Blyth offshore wind farm in 2000 and the 60MW Hoyle offshore wind farm in 2003 – both closed with 100% utility ownership by E.ON and RWE, respectively.

The graph below shows how utilities took the lion’s share of the equity on the first five projects charted in IJGlobal’s database, which reached close between 2000 and 2012.

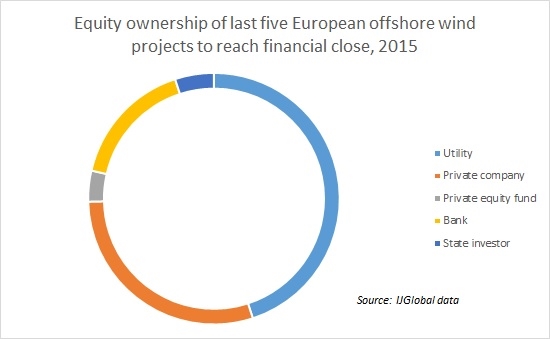

Since then, the number of projects, and equity players, has risen sharply. The two most recent financial close transactions on IJGlobal’s database brought corporates, equity houses, private banks and the UK's Green Investment Bank, which did not even exist five years ago, into their equity consortia. The £1.54 billion ($2.35 billion), 336MW Galloper and the €650 million ($716.1 million), 165MW Belwind 2 project – demonstrate offshore wind developments as an increasingly competitive and attractive arena for a broad range of investors.

The graph below demonstrates a typical equity model seen in recent offshore wind developments. Utilities are still the primary developer of the projects, but they are selling off stakes to a growing pool of investors before, or at, financial close.

The equity groups have arguably become more sophisticated as the technology has improved and completed projects have had the chance to prove themselves. Investors, too, have been attracted by state subsidy schemes, particularly in Germany and the UK, and long-dated returns linked to power purchase agreements.

Recent ownership models also reflect the struggling finances of many European utilities and their evolution from vertically integrated one-stop-shops of a decade ago to the fragmented, spun-off separate businesses they have become today.

Projects owned solely by utilities at financial close in 2015 – such as WPD's Nordergreunde – appear more likely to have had 100% utility ownership at financial close by accident rather than design. Nordergruende had been in the market looking for equity partners, which it failed to find before financial close.

Utilities are making clear that this wider ownership model is set to stay. DONG Energy and Mainstream, for example, have both set out plans to sell off equity stakes at financial close for their upcoming projects, such as Mainstream's Neart na Gaoithe in the UK. Scottish utility SSE is in active talks to sell off an equity share in its £1.95 billion Beatrice project, as IJGlobal exclusively reported earlier this week. It has already sold shares to Copenhagen Infrastructure Partners.

And as the equity stakeholders become more diverse, so too do their methods of deploying equity capital into projects. Global Infrastructure Partners (GIP) issued €550 million ($621.7 million) in project bonds in October to buy a 50% stake in Dong Energy’s Gode Wind 1 offshore wind farm in Germany.

GIP will part-fund the €780 million acquisition by issuing the non-recourse, investment grade certified green bonds to a consortium of German insurers.

Next month's 700MW Dutch offshore wind tender will likely draw in a broad mix of equity investors. Capital providers are expected to join the tender competition, with one bank saying there is “likely to be a face-off between these and the utilities.” Dutch pension fund APG has already said it is looking at the development.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.