Data Analysis: US toll roads on sale

A couple of high profile acquisitions of real toll road leases in the US during 2015 and 2016 attracted attention for the high equity values involved - the Indiana Toll Road and the Chicago Skyway. With the market shown to be liquid for these types of vital transport assets, IJGlobal has learned that several other sales of US toll road leases are underway.

IJGlobal reported exclusively last week that Macquarie Infrastructure Partners (MIP), the first generation MIP fund dating to 2007, has launched teasers for the sale of its 50% share of the Dulles Greenway in Virginia.

The sale of the Pocahontas Parkway in Virginia is very close to preferred bidder stage, with an announcement anticipated by the end of September. The vendors are Macquarie Corporate & Asset Finance, TPG Capital and Citigroup. IJGlobal understands they received three final bids.

The Northwest Parkway meanwhile, also known as the Denver Beltway, is 100% owned by Portuguese concession company Brisa and IJGlobal understands that the second round of a sale process for that asset is underway. A spokesperson for Brisa has confirmed that Moelis was mandated as financial adviser and that “selling is within all strategic options under consideration by Brisa for the Northwest Parkway Concession”.

The State Highway 130 Concession Company, owned by Spanish developer Cintra and Texas-based Zachary American Infrastructure, filed for Chapter 11 bankruptcy in the Western District of Texas in March this year. Then on 12 August the company submitted a restructuring plan, calling for SH130 to be brought “under new ownership”, whereby the project lenders would own all membership interests. The concession company said it hopes to announce a resolution in the “coming months”. Lenders could be reasonably expected to seek a sale at some point thereafter to recoup their credit.

Why sell now?

There have been several factors driving the sales of private sector-owned US toll roads.

Macquarie’s MIP fund, which is one of the earlier infrastructure funds, is seeking to sell its shares in Dulles Greenway as it approaches maturity in March 2017.

The Chicago Skyway and Indiana Toll Road are decades old, but in 2006 both were leased to the same private investors: Cintra and Macquarie. Both assets were negatively impacted by aggressive financial structures set up at that time, with accreting swaps to lower early debt service payments and high leverage, and Indiana Toll Road ended up in bankruptcy in September 2014.

There is a well-documented history of over-optimistic forecasts for traffic volumes globally, including the US market, especially after assumptions regarding gross domestic product growth and regional development were dashed by the global financial crisis beginning in 2008. Financial models began to breakdown as the gap between traffic volumes and forecasts widened.

Toll roads entering operations in the last three to five years, however, have performed closer to forecasts, explains Cherian George, managing director of Americas infrastructure at Fitch Ratings.

And for some historically troubled toll roads, the market for financing acquisitions is healthy.

George says: “My sense is that some of these assets have demonstrated tremendous underlying strength and that is what’s driving these owners to take advantage of the current environment: low interest rates and a lot of equity chasing few assets… I think it has a lot to do with timing. Who knows how long the low interest rate environment will continue, and investor appetite can change quite dramatically depending on global events, so this might be the best time for the current owners to maximise their returns.”

Buyers for the Indiana Toll Road in 2015 and Chicago Skyway in 2016 have been backed with pension fund and insurance capital looking for long-term investments. For Chicago Skyway, the buyer was a consortium of three Canadian pension funds, while for Indiana Toll Road it was IFM Investors, which manages the capital of over 70 US pension funds in its Global Infrastructure Fund, with co-investors CalPERS and Allstate Corporation.

Reports of multiples above 30x earnings before interest, tax, depreciation and amortisation (Ebitda) for Indiana Toll Road and Chicago Skyway, attest to high levels of equity from funds competing fiercely. But regarding the debt for those acquisitions George said: “We are rating the debt and the debt is usually at multiples between 10x and 15x [Ebitda]. The leverage on the debt is about 10x to 15x which is much more within a range that seems reasonable historically.”

Asked whether the handful of upcoming sales are likely to command a similar level of enthusiasm, George suggests: “You have very strong assets like Indiana Toll Road, a strong asset like Chicago Skyway, a strong asset like the Dulles Greenway. But then Northwest Parkway … is performing well, toll rates are high [and] Denver is a growing area. But [it] has a very limited service area as it’s defined today, which means you should not in theory have the same multiples. The value to be gained long term is much more speculative.”

Limited pool

While there is appetite in the private sector, there isn’t a large number of real toll roads in the US market that are candidates for buying.

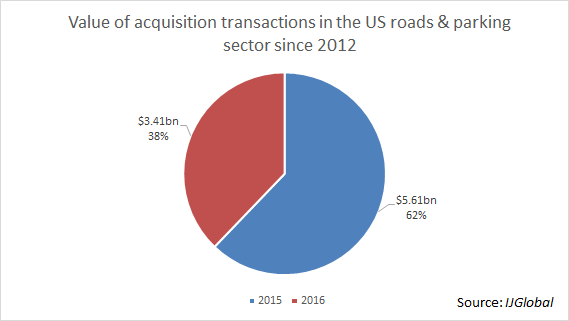

IJGlobal’s data records only five asset acquisitions in the roads/parking sector completed since 2012, all taking place in 2015 and 2016.

There is not a large number of toll roads in private ownership in the country, and it is unlikely, George attests, that further roads would come out of public hands soon.

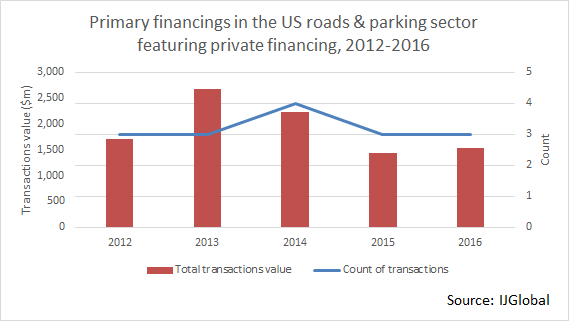

IJGlobal’s data shows only 16 completed private sector, primary financing transactions for US toll roads, availability-based road concessions, managed lanes projects and parking concessions since 2012. IJGlobal’s data records only five asset acquisitions in the roads/parking sector completed since 2012, all taking place in 2015 and 2016.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.